The Edges of Finance

The Bank for International Settlements (BIS) recently published a paper on DeFi lending. It starts off with some provocative framing:

Given the need for over-collateralisation in DeFi lending (contrary to what happens in traditional banking), it is somewhat surprising that any borrowing activity takes place on these platforms at all.

We should all be excited (seriously!) that the BIS is paying its economists to study DeFi. Papers like this genuinely help legitimize the space over time, as does the experimental work the BIS Innovation Hub has undertaken (see Project Mariana). That said, we should also take a step back and offer a broader perspective when papers from outside the crypto industry are narrowly focused. Staff research from an important institution is often (understandably) interpreted as official policy. When it skews to the negative, it can have a significant impact on the willingness of others to engage.

Using bank lending as a starting point for analyzing DeFi lending ignores the unique characteristics of each form of lending. It also suggests that banks have an impenetrable moat around credit intermediation without acknowledging the broader backdrop of technical and social change at the edges of the global financial architecture.

Collateralization is a spectrum that balances risk, liquidity, and capital efficiency

Banks are structurally risky, as we saw in March 2023. Maturity mismatch necessarily leads to instability, which is why central banks and prudential regulation exist in the first place. The capital efficiency we get through uncollateralized bank lending is socially costly and operationally difficult to control.

In recent years, there has been a surge in collateralized borrowing in private credit markets. These products often come with covenants that allow creditors to claim assets in the case of a borrower default. (More on this below.)

For example, we see what looks a lot like overcollateralization in the market for repurchase agreements, known as the repo market. When Alice and Bob agree to an overnight repo trade, Alice gives Bob $100 cash in exchange for $100 in treasuries. The next day, Bob pays back Alice the $100 plus some interest, and Alice returns to Bob his $100 in Treasuries.

Given the need for a very high collateral-to-loan ratio in repo, it may be surprising that any borrowing happens in the repo market at all. However, the US repo market alone handles roughly 4 trillion USD in trading volume everyday. The numbers have increased in recent years. In fact, the Federal Reserve now runs a number of repo facilities that are always available for a subset of the financial system to use to source cash or securities. Many institutions use the repo market to obtain leverage for trading, similar to how crypto traders use crypto lending markets to fund profitable trades (this works in part because many traders experience significant capital gains, which blunts the capital impact of overcollateralization).

Overcollateralization in crypto is partly due to the fact that crypto markets are volatile — but the current model works for its intended purpose. While there may be some exceptions, the target customer for DeFi lending today is not the same as bank lending. That may change in the future as the industry evolves to meet the changing needs of its users; but today, the average Aave user is not seeking an Aave loan to buy a house, much like the average repo user is not using the repo market to fund consumer purchases.

Financial services are increasingly shifting away from banks (regardless of what happens in crypto)

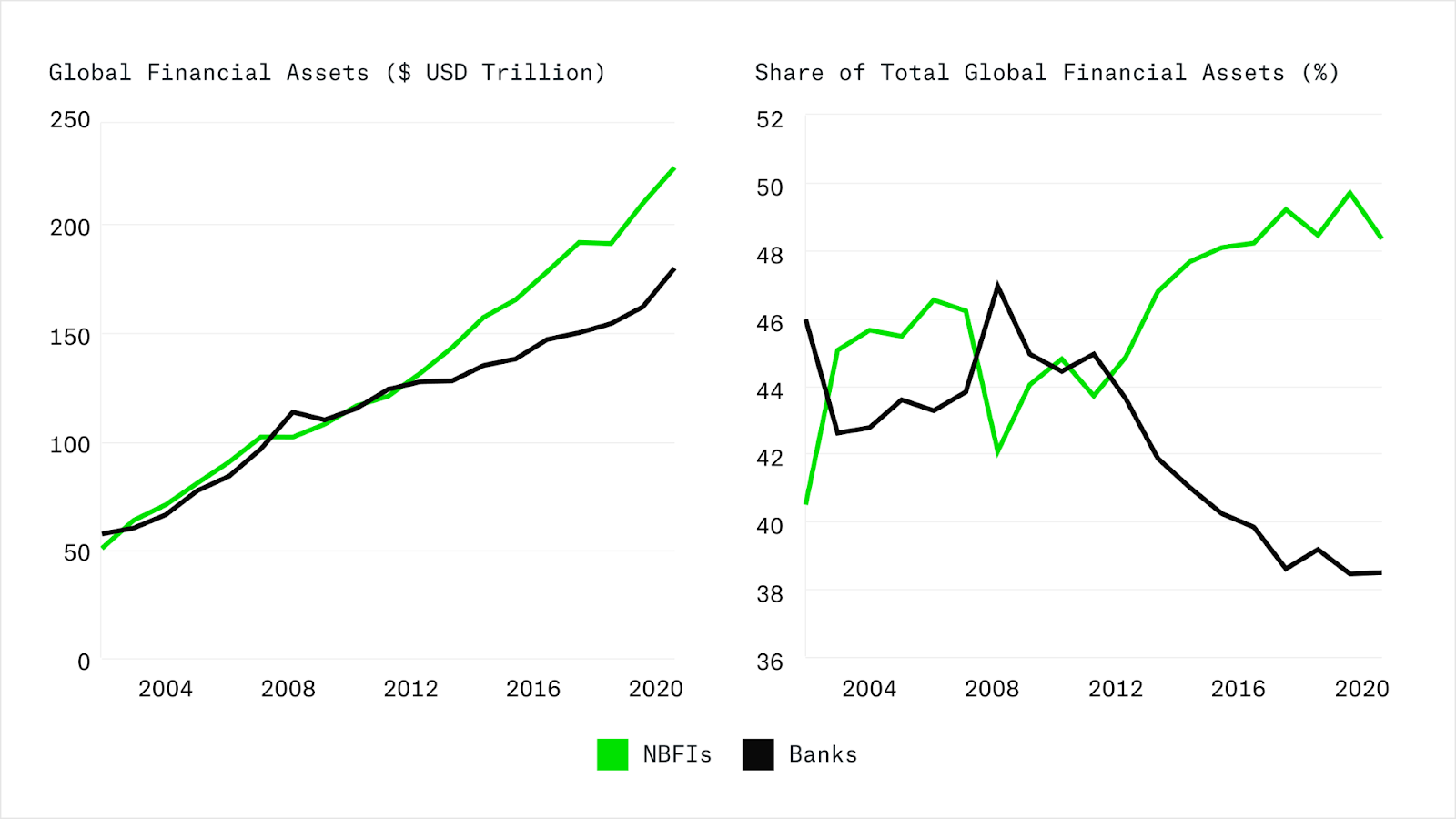

Banks are still an important part of the financial system, both literally and in terms of social perception, but the size and scope of their activities has changed significantly in the past 20 years. The rise of DeFi lending follows a well-documented trend of banks ceding ground to new entrants in a variety of verticals.

Since 2008-09, there has been a dramatic increase in nonbank financial institutions – in aggregate and in share relative to banks. Much of this is a result of post-crisis regulation that disincentivizes banks from growing in size and complexity. This means that banks have had to curtail their activities and that non-banks have stepped up to fill the void.

Here is a set of charts from the New York Fed that show just how important nonbanks have become over the last decade. The Financial Stability Board has also been documenting this trend in near real time.

Private credit is going through a particularly large boom right now. According to estimates from the Fed, direct lending via private credit has grown from almost nothing in 2008 to an $800 billion market today. These are mostly term loans, originated by nonbanks, with various degrees of collateral backing them. Private credit differs from collateralized DeFi lending in at least one important respect. While private credit avoids the duration mismatch problem that arises in bank-intermediated lending, it relies on mostly illiquid collateral as opposed to most DeFi lending today which is predicated on the ability to liquidate collateral as needed.

The thing to underscore is that while banks are still very important, they are not the locus of innovation in finance today. After a financial crisis that roiled banks, regulators and the private sector responded by redesigning the system to push some forms of credit intermediation out of the core and into other parts of the financial system. Lending is getting narrower, even if you strip out all of the activity happening in crypto markets.

This is why it is difficult to grok some of the critiques about DeFi lending that come off as less serious about what it is and more concerned with what (or where) it is not (e.g., banks).

As activity moves out of the core and toward the edges, having a unified (verifiable) representation of the state of the system becomes more important

By now, most people know that cash is ceding ground to digital payments as countries like the US (FedNow and RTP), Brazil (Pix), and India (UPI) are moving to faster/instant payments systems — all while activity is shifting out of banks. At some point, these fragmented systems, which are constantly increasing in number and capabilities, need to be able to talk to each other.

The BIS acknowledges this and grants that improvements in technology warrant larger changes in how the financial system functions and interoperates. In a recent op-ed, the General Manager of the BIS wrote:

Financial services must catch up with the advances made in communications since the advent of the internet and smartphones. That will require taking bold action to build a seamless, interconnected network that would give all individuals and businesses full control over their financial lives.

Ethereum and other blockchains are already serving this purpose. Stablecoins and real-world assets (RWAs) on public blockchains are some of the first TradFi-legible examples of how a global state machine can be used to represent financial services. We have seen that over time, even the large institutional players are converging on a global standard that is anchored to the crypto community. Rapidly, many of the concerns that policymakers once flagged about the use of public blockchains in finance (scalability, key management, operational risk) are being resolved by technologists.

It is possible that all of the moving parts of finance, across markets, entity-types, and jurisdictions come together on a closed but interconnected platform that is extensible enough to meet all of their needs. But it does not seem very likely. If you look at some of the most successful fintech companies of the last 20 years, many today are the middleware that connects disparate, non-interoperable systems.

What seems more likely, at least in the short run, is that institutions and innovators meet in the middle and build on top of systems that are open and easy to use — and already live.

Record scratch: Crypto is about more than simply recreating existing financial primitives

This is the most-important observation of all.

It is easy to get frustrated in the face of challenges to crypto and public blockchains that boil down to “it would be too risky to do this [systemically important/socially enshrined] activity today on a public blockchain,” but they are orthogonal to the pulse of social and technical change.

Crypto is a long-term project. Part of the project involves upgrading existing systems for social coordination — including money and finance — using a new set of technologies that empower users and are open and accessible. Another part of the project involves creating entirely new things that might look kind of like old things but only if you squint hard enough.

Pushing the frontier means products and services that seem insane until they are obvious.